Exploring the History, Performance, Regulatory Frame work and the future outlook of Collective Investment Schemes in Uganda

Collective Investment Schemes (CIS) were introduced in November 2003, by the Collective Investment Schemes Act, with the first unit trust being established by African alliance around 2005. The industry has since grown, with various players entering the market. Currently there over 6 fund managers and 91,289 funded investor unit trust accounts.

However there has been Challenges limiting growth, for example, Limited investor education and awareness, Low penetration of CIS in rural areas, Dependence on traditional assets (e.g., land and property), Regulatory challenges (e.g., tax implications, investor confidence, licensing requirements, disclosure requirements, kyc).

Performance:

Adoption by the Public:

1. Growing awareness and interest in CIS

2. Increase in individual investors (Currently 91,289 funded investor unit trust accounts with total Assets Under Management (AUM) of up to ugx 3 trillion)

3. Expansion of distribution channels (banks, online platforms, investment websites, social media)

Total Assets Under Management (AUM):

1. 2019: UGX 389 billion (approx. USD 102 million)

2. 2020: UGX 440 billion (approx. USD 115 million)

3. 2021: UGX 978 billion (approx. USD 257 million)

4. 2022: UGX 1,629 trillion (approx. USD 428 billion)

5. 2023: UGX 2,357 trillion (approx. USD 620 billion)

6. 2024: UGX 3,079 trillion (approx. USD 810 billion)

Collective investment schemes have grown averagely by 209% year on year since 2019 to June 2024.

Average Interest Rates:

1. Money Market Funds: 8% – 11% per annum

2. Umbrella Funds: 10% – 12.5% per annum

The Regulatory Framework of Collective Investment Schemes

Uganda’s regulatory framework for collective investment schemes (CIS) is primarily governed by the Collective Investment Schemes Act, 2003, and regulated by the Capital Markets Authority (CMA), The framework allows for both open-ended investment companies (OEICs) and unit trusts schemes, but currently, only unit trusts are operational. Some of the Key Regulatory Requirements include;

- Licensing: Collective investment schemes must be licensed by the CMA

- Disclosure: Schemes must provide investors with regular reports and disclosures

- Investment Restrictions: Schemes are restricted from investing in certain assets or sectors

Safety of Schemes:

1. Regulatory oversight by CMA

2. Segregation of assets

4. Regular audits and reporting

5. Compliance with international standards (e.g., IFRS)

Investor Protection:

These measures aim to ensure transparency, accountability, and investor protection in Uganda’s collective investment scheme market.

1. Capital Markets Authority (CMA) ensures compliance with regulations

2. Independent trustee oversight.

3. Investor Compensation Fund (ICF) established

4. Disclosure requirements for CIS

5. Regular inspections and monitoring

6. Education and awareness initiatives

The Future of Collective Investment Schemes.

The future of collective investment schemes (CIS) is shaped by evolving investor preferences, technological advancements, and regulatory changes. Here are trends and innovations influencing the future of CIS, focused on investor buying behaviours’:

Trends:

1. Sustainable Investing: Growing demand for ESG (Environmental, Social, and Governance) investments.

2. Digitalization: Online platforms, mobile apps, and digital distribution channels.

3. Passive Investing: Increased adoption of index funds and ETFs.

4. Alternative Investments: Rising interest in private equity, real estate, and cryptocurrencies.

5. Personalization: Tailored investment solutions and model portfolios.

Innovations:

1. Artificial Intelligence (AI): AI-driven investment advice and portfolio management.

2. Blockchain: Enhanced security, transparency, and efficiency in CIS operations.

3. Robo-Advisory: Automated investment advice and portfolio rebalancing.

4. Micro-Investing: Fractional investing and low-cost, subscription-based models.

5. Impact Investing: Investments targeting specific social or environmental outcomes.

Investor Buying Behaviours:

1. Increased demand for transparency and disclosure.

2. Growing interest in thematic investing (e.g., healthcare, fintech).

3. Preference for low-cost, index-tracking funds.

4. Desire for personalized investment advice and portfolio management.

5. Rising importance of ESG considerations.

Future Outlook of Collective Investment Schemes in Uganda.

1. Growing demand for mobile-based investment platforms.

2. Increasing adoption of ESG considerations.

3. Regulatory support for innovation and fintech.

4. Expanding investor education initiatives. (Social Media)

5. Rising interest in alternative investments.

6. Increased adoption of digital platforms

7. Expansion of CIS offerings (e.g., Shariah-compliant funds)

8. Growing demand for alternative investments (e.g., private equity)

9. Strengthened regulatory framework

Future Outlook of Collective Investment Schemes on a Global Market.

1. Hybrid Models: Combining human expertise with AI-driven insights.

2. Open Architecture: Integration of multiple asset managers and platforms.

3. Fee Compression: Pressure on fees due to passive investing and digital distribution.

4. Regulatory Evolution: Adaptation to emerging trends and technologies. Guidance on financial social media Promotions and Democratization of Retail Investing.

5. Globalization: Increased cross-border investments and collaborations.

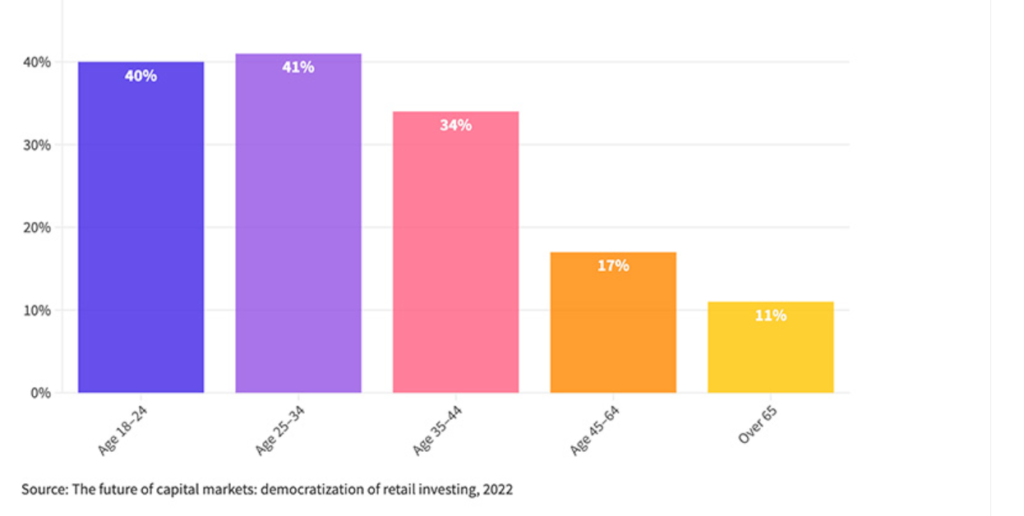

Age of retail investors around the world turning to social media for investment advise 2022

It’s clear that financial engagement is changing. But how are people choosing to engage with financial advice, and is their financial literacy sufficient to realise the full potential of wealth creation without falling prey to misleading information?